OLD FUNDAMENTAL FORECAST: BULLISHTALKING POINTS:

Gold charge notches its first weekly decline in over a month

US-China change struggle trends boosted chance-on sentiment

Strong US production information driven the USD better notwithstanding Fed turning Dovish

The charge of Gold has stumbled decrease during the last week as hazard-on sentiment precipitated fading investor call for for the treasured metallic. Since Gold is frequently checked out as a secure-haven asset that buyers can flip to at some point of instances of heightened uncertainty, latest inventory marketplace optimism and a sturdy US Dollar contributed to the bright metallic’s zero.five percentage decline due to the fact that final Friday.

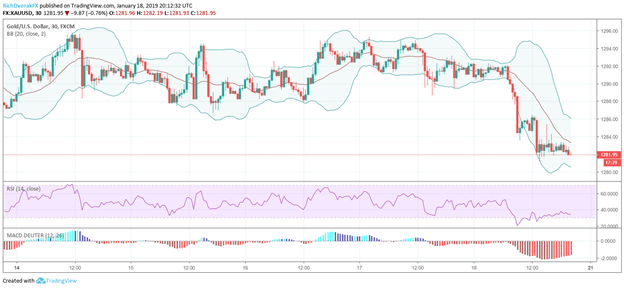

GOLD PRICE CHART: 30-MINUTE TIMEFRAME (JANUARY eleven, 2019 TO JANUARY 18, 2019) (CHART 1)

The drop in Gold’s charge over the past five buying and selling days snapped the commodity’s streak of four consecutive weeks of profits. While Gold became buying and selling sideways for maximum of the closing week, rate movement on January 18 noticed a widespread zero.eight percentage dip in XAUUSD wiping out all profits revamped the earlier few days.

The decline in Gold become as a consequence of chance belongings rejoicing on reviews that China can also remove its exchange deficit with the US inside the state-of-the-art ploy to slow down the USA-China alternate struggle and raise marketplace self assurance. The information comes after an exciting week inside the economic markets surrounding Brexit drama, america authorities shutdown, and blended financial trends round the sector.

Most extensively, weaker than anticipated facts out of China caused the u . S .’s leaders stepping up its willingness to help its worsening financial system. Chinese officers introduced file-breaking liquidity injections and a decreasing of the USDCNY solving from 6.9709 on the give up of remaining week to six.7560 on Monday while the terrible facts turned into launched. Due to the robust correlation among XAUUSD and CNYUSD, this to start with helped push Gold better.

USDCNY, DXY, XAUUSD PRICE CHART: 15-MINUTE TIMEFRAME (JANUARY eleven, 2019 TO JANUARY 18, 2019) (CHART 2)

However, this improvement changed into negated during the week as superb readings on financial information on US housing, jobless claims, commercial enterprise outlook and production despatched the DXY marching better regardless of greater dovish feedback from Federal Reserve officers.

Looking beforehand to subsequent week, the forecast for Gold stays bullish because the essential thesis for capability advances stays in tact. If fantastic alternate speak traits in addition materialize, this can upload aid to a faltering Chinese economic system and bolster its home forex. In flip, this can role Gold for in addition upside. Moreover, the lingering dangers that decrease GDP poses to shares similarly to the hazard a dovish Fed poses to the Dollar – each a number one end result from an prolonged US Government Shutdown – is more and more commonplace. Downside dangers to the forecast highlights extra profits inside the USD or devaluation within the CNY similarly to similarly chance-on sentiment ensuing in investors overlooking Gold.

Gold Weekly, Fundamental ,Outlook: ,USD ,Gains and Returning ,Optimism ,Fade